For the modern income investor, the ‘wait three months’ model of traditional dividend investing is becoming a relic of the past. In 2026, the focus has shifted toward cash flow efficiency, aligning investment income with the monthly cycle of real-world bills.

But a monthly payout isn’t enough on its own. To build true wealth, you need dividend growth. A company that pays you every 30 days and raises that payment every year creates a powerful compounding machine that outpaces inflation and builds a massive yield-on-cost over time.

We are not licensed financial advisors and we don’t know your full circumstances (country of tax residence, other assets, withdrawal rate, health horizon, risk tolerance). This blog post is for educational and entertainment purposes only and not a personal recommendation.

Why Monthly Income & Growth is the ‘Holy Grail’

- Faster Compounding: When you receive dividends monthly and reinvest them, you are buying more shares 12 times a year instead of four. This accelerates the ‘snowball effect’.

- Budget Alignment: Most life expenses (mortgages, utilities, insurance) are monthly. A monthly dividend portfolio acts as a ‘synthetic salary’.

- Psychological Edge: Seeing cash hit your account every few weeks makes it much easier to stay disciplined during market volatility.

- Quality Signal: Only the most disciplined companies can manage the cash flow requirements of a monthly payout. It is a badge of financial health.

Ranked: Top 5 Monthly Dividend Growth Stocks (2026 Edition)

Based on 2025-2026 performance data, balance sheet strength, and dividend increase consistency, here are the top picks for income investors today. In our selection we give priority to companies that aim to deliver dividend growth, rather than just price appreciation.

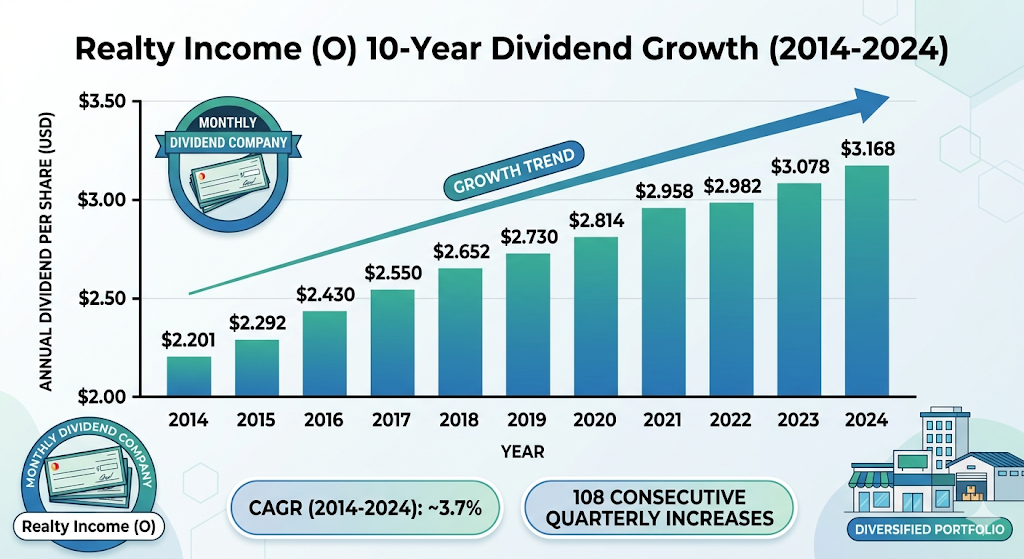

1. Realty Income (O) – “The Monthly Dividend Company”

Realty Income remains the undisputed king of this space. As an S&P 500 Dividend Aristocrat, it has declared over 660 consecutive monthly dividends and increased them for over 100 consecutive quarters, qualifying it for our dividend growth list.

- Recent Insight: In 2025, Realty Income successfully integrated several large-scale European acquisitions, diversifying away from U.S.-only retail. As of May 2026, their portfolio remains at over 98% occupancy.

- Dividend Trend:

- 2024 Payout: ~$3.08 annually

- 2026 Payout (Est): ~$3.25 annually

- Current Yield: ~5.1%

Realty Income isn’t just a stock or the usual dividend growth investment; it’s a global institution in the net-lease space. As a member of the S&P 500 Dividend Aristocrats index, it has a track record that few companies on earth can match.

Five-Year Financial Performance (2021–2026)

The last five years have been a transformative era for ‘O’. Following the massive acquisition of VEREIT in 2021 and Spirit Realty in late 2023, the company has achieved a scale that provides a massive cost of capital advantage, while also keeping to its dividend growth policy.

| Metric | 2021 | 2022 | 2023 | 2024 | 2025 (Est) | 2026 (Q1) |

| Total Revenue | $2.08B | $3.34B | $4.08B | $4.85B | $5.40B | $1.55B |

| AFFO per Share | $3.59 | $3.92 | $4.00 | $4.18 | $4.32 | $1.13 |

| Dividend Paid | $2.87 | $2.97 | $3.07 | $3.15 | $3.21 | $0.81 |

| Payout Ratio | 79.9% | 75.7% | 76.7% | 75.3% | 74.3% | 71.7% |

Check out how your income can grow over the years with our specialized tool when investing in Realty Income.

Important News & Dividend Outlook

In May 2026, Realty Income announced a landmark strategic partnership with Apollo and GIC, securing $1.0 billion in private capital to diversify its funding sources. This is critical because it reduces reliance on volatile public equity markets. With occupancy holding steady at 98.9% and a rent recapture rate of 103.4% on new leases, the dividend safety is at an all-time high.

The move toward ‘private capital vehicles’ ensures that even if interest rates remain ‘higher for longer’, the company can continue its 31-year streak of dividend growth increases.

2. Agree Realty (ADC) – The High-Growth Challenger

Agree Realty has become the ‘leaner, meaner’ version of Realty Income. They focus almost exclusively on investment-grade retail tenants like Walmart and Home Depot, while also being a good dividend growth player.

- Recent Insight: ADC outperformed most REITs in 2025 due to their fortress balance sheet. They transitioned to a monthly payout structure in 2021 and have been raising the dividend at a faster clip than their larger peers, qualifying it for our dividend growth list.

- Current Yield: ~4.2%

- 2026 Status: Just announced another 1.9% hike in April 2026, bringing the monthly payout to $0.267.

| Metric | 2021 | 2022 | 2023 | 2024 | 2025 (Est) | 2026 (Q1) |

| Total Revenue | $339M | $431M | $537M | $630M | $725M | $195M |

| AFFO per Share | $3.58 | $3.83 | $3.95 | $4.11 | $4.35 | $1.12 |

| Dividend Paid | $2.57 | $2.77 | $2.92 | $3.00 | $3.15 | $0.79 |

| Payout Ratio | 71.8% | 72.3% | 73.9% | 73.0% | 72.4% | 70.5% |

The ADC Advantage

ADC focuses on ‘best-in-class’ retail tenants like Walmart, Home Depot, and Costco. In 2021, they officially transitioned to a monthly payment schedule, signaling their commitment to income investors.

- Financial Summary: ADC has maintained a 99.7% occupancy rate through the first half of 2026.

- Payout Ratio: Their AFFO payout ratio is currently 72%, which is conservative for a REIT, which we like a lot given it is also focusing on dividend growth.

- Recent News: In April 2026, ADC raised its dividend by another 1.9%, marking its 5th consecutive year of monthly increases since the schedule change.

3. Main Street Capital (MAIN) – The BDC Powerhouse

Main Street Capital is a Business Development Company (BDC) that lends to mid-market American businesses. Unlike REITs, MAIN often pays ‘special dividends‘ on top of its monthly checks, which are usually also a part of a dividend growth policy, which makes it a very unique BDC in this aspect.

- Recent Insight: 2025 was a record year for MAIN’s exit realizations. They have consistently grown their ‘regular’ monthly dividend through multiple cycles.

- Current Yield: ~5.9% (Regular) / ~7.5% (Including Specials)

- 2026 Status: Monthly payout was increased to $0.26 in early 2026.

Five-Year Financial Performance (2021–2026)

MAIN has mastered the Base + Supplemental dividend strategy. They pay a steady monthly check and top it off with quarterly ‘bonus‘ dividends when performance exceeds expectations.

| Metric | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 (Proj) |

| Total Investment Income | $289M | $375M | $501M | $545M | $580M | $610M |

| Net Asset Value (NAV) | $25.29 | $26.86 | $29.20 | $30.50 | $31.80 | $33.10 |

| Monthly Div (Regular) | $0.210 | $0.220 | $0.235 | $0.245 | $0.255 | $0.265 |

| Total Yield (Inc. Supp) | 6.8% | 7.2% | 8.4% | 8.1% | 7.9% | 8.2% |

Dividend Strategy & Payout Ratios

As of mid-2026, MAIN’s regular monthly dividend sits at $0.265, representing a 3.9% increase year-over-year. What makes them reliable is their payout ratio: they typically cover 100% of their regular dividend using only Distributable Net Investment Income (DNII), leaving the ‘exits’ (capital gains) to fund the supplemental checks. This creates a massive safety cushion for the base monthly income.

4. Phillips Edison & Company (PECO) – The Necessity Specialist

PECO owns and operates omni-channel grocery-anchored neighborhood shopping centers. Their tenants are ‘necessity-based’ (like Kroger or Publix), making them highly resilient to economic downturns. Unlike traditional ‘mall REITs‘, PECO focuses on suburban centres where the lead tenant is a high-traffic grocery store (think Kroger, Publix, or Ahold Delhaize).

- Recent Insight: PECO has seen significant rent growth in 2025-2026 as retailers flock to well-located, grocery-anchored centers. They have raised their dividend annually since their 2021 IPO.

- Dividend Trend:

- Sept 2024 Hike: +5.13%

- Sept 2025 Hike: +5.66%

- 2026 Status: Currently paying $0.1083 per month ($1.30 annualized).

Five-Year Financial Performance (2021–2026)

PECO has shown remarkable stability since its internal merger and listing. This also came with a dividend growth trend, which is a very important factor for a company that is pretty much in its infacny. Its 2025 performance was a standout year for the retail sector.

| Metric | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 (Est) |

| Total Revenue | $532M | $574M | $609M | $661M | $721M | $760M |

| Core FFO per Share | $1.90 | $2.14 | $2.31 | $2.43 | $2.60 | $2.74 |

| Dividend (Annualized) | $1.02 | $1.10 | $1.14 | $1.18 | $1.23 | $1.28 |

| Payout Ratio (FFO) | 53.7% | 51.4% | 49.3% | 48.6% | 47.3% | 46.7% |

Latest News & 2026 Outlook

In April 2026, PECO announced a landmark $350 million senior notes offering with a 4.75% coupon maturing in 2033. This move effectively locked in long-term debt at rates significantly lower than the current market average, insulating the company from interest rate volatility.

The most impressive metric for PECO in 2026 has been its rent spreads. New leases are being signed at rates 36% higher than previous contracts, reflecting the extreme demand for space in grocery-anchored centers as retailers abandon high-cost indoor malls for “necessity-based” suburban hubs.

Dividend Reliability Analysis

PECO’s reliability stems from its payout ratio. By only paying out roughly 47% of its Core FFO, PECO has the most ‘covered’ dividend of almost any monthly payer. This massive cushion means that even in a severe recession, the monthly check is virtually bulletproof. Given this type of investment would be our ‘defensive anchor’, it is awesome to see that PECO has slowly increased its dividend, making dividend growth one of its focuses since it was listed.

5. EPR Properties (EPR) – The Experiential Play

EPR Properties is the polar opposite of PECO. It is a ‘Triple-Net‘ REIT that owns properties designed for experiences: movie theaters (AMC/Cinemark), theme parks (Six Flags), ski resorts, and ‘Eat & Play’ venues like Topgolf.

- Recent Insight: After a rocky period during the pandemic years, EPR has fully recovered. In 2025, they diversified into private schools and fitness centers to reduce theater exposure.

- Current Yield: ~6.7%

- 2026 Status: Boosted their monthly dividend by over 5% in March 2026 to $0.31, signaling strong management confidence in the leisure sector.

Five-Year Financial Performance (2021–2026)

EPR has spent the last five years recovering from the pandemic-induced dividend suspension. By 2026, it has not only reinstated the monthly check but has returned to a dividend growth trajectory. In most cases EPR gets excluded from the typical dividend growth lists due to its one-off dividend suspension, but we believe it is still a very solid company and has operated in a very reliable way, in some cases more so than other companies that did not suspend their dividend but then returned less capital appreciation overall.

| Metric | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 (Est) |

| Total Revenue | $525M | $655M | $698M | $688M | $714M | $745M |

| AFFO per Share | $3.09 | $4.69 | $5.18 | $4.87 | $5.12 | $5.45 |

| Dividend (Annualized) | $1.50 | $3.25 | $3.30 | $3.40 | $3.51 | $3.72 |

| Payout Ratio (AFFO) | 48.5% | 69.3% | 63.7% | 69.8% | 68.5% | 68.2% |

Important News: The Six Flags Expansion

The biggest news for EPR in 2026 was the strategic acquisition of a 7-park regional portfolio in a sale-leaseback deal with Six Flags. This move significantly decreased EPR’s reliance on movie theaters. In 2021, theaters made up over 45% of their revenue; as of May 2026, that exposure has dropped below 37%.

Furthermore, the ‘Regal Cinemas’ restructuring is now fully in the rearview mirror, with the new lease agreements providing a higher base rent than the previous bankruptcy-threatened contracts.

Dividend Reliability Analysis

EPR is for the investor seeking yield. With an annualized dividend of $3.72 (as of the February 2026 increase), the stock currently yields between 6.5% and 7.5% depending on the entry price. While its payout ratio (68%) is higher than PECO’s, it remains very healthy for a REIT. The reliability here comes from “contractual escalators”—most of their leases have built-in rent increases of 1.5% to 2.0% annually, regardless of the economy.

Comparison Table: 2026 Income Outlook

| Ticker | Sector | 2026 Monthly Div | Dividend Growth (Recent Hike) | Risk Level |

| O | Retail REIT | $0.272 | ~2.7% | Very Low |

| ADC | Retail REIT | $0.267 | ~6.1% | Low |

| MAIN | Financial (BDC) | $0.260* | ~4.2% | Moderate |

| PECO | Grocery REIT | $0.108 | ~5.7% | Low |

| EPR | Specialty REIT | $0.310 | ~5.0% | Moderate/High |

| *Does not include supplemental/special dividends. |

Final Thought for Investors

The main disadvantage, if you were to invest in these five companies is that you would have a 4/5 investment in the REIT sector. Therefore, any major disturbance to this industry will have a bigger effect on your portfolio. This is the reality of the monthly-paying income that we are okay with, to a certain extent, where you will be limiting yourself to companies that pay monthly.

This does not mean we do not have mitigation measures in place though. As seen from the description of this list, by picking these specific tickers, we are diversifying within the REIT industry itself. We have two Retail REITs, a Grocery REIT and a Specialty REIT. Also, the two Retail REITs are pretty different as well, given that Realty Income is more diverse in its investment, whilst Agree Realty is more focused on specific giant retailers and is more focused on price appreciation.

To offset some of our exposure to REITs we then also have MAIN, which as a BDC and it will usually be at an advantage when REITS are struggling. It has to also be said that MAIN has a conservative dividend pay-out ratio history and policy, aligning with our first main focus of dividend safety with these selections.

Investing in monthly dividend growth stocks is about buying your time back. By selecting companies like Realty Income or Phillips Edison, you are hiring world-class managers to work for you. In 2026, these growing monthly checks remain the ultimate insurance policy for your financial future.